How to financially prepare for life after graduation

If you're a student who's approaching graduation, you’re probably busy wrapping up finals, job hunting, and hopefully enjoying your last couple months of student life before entering the “real world”. Whether you’re attending a trade school or four-year college, in the midst of everything else you may have some concerns about affording life after graduation; from rent to loans and car payments, expenses can add up quickly. Preparing financially for post-grad life means doing your research, planning ahead, and saving money where you can.

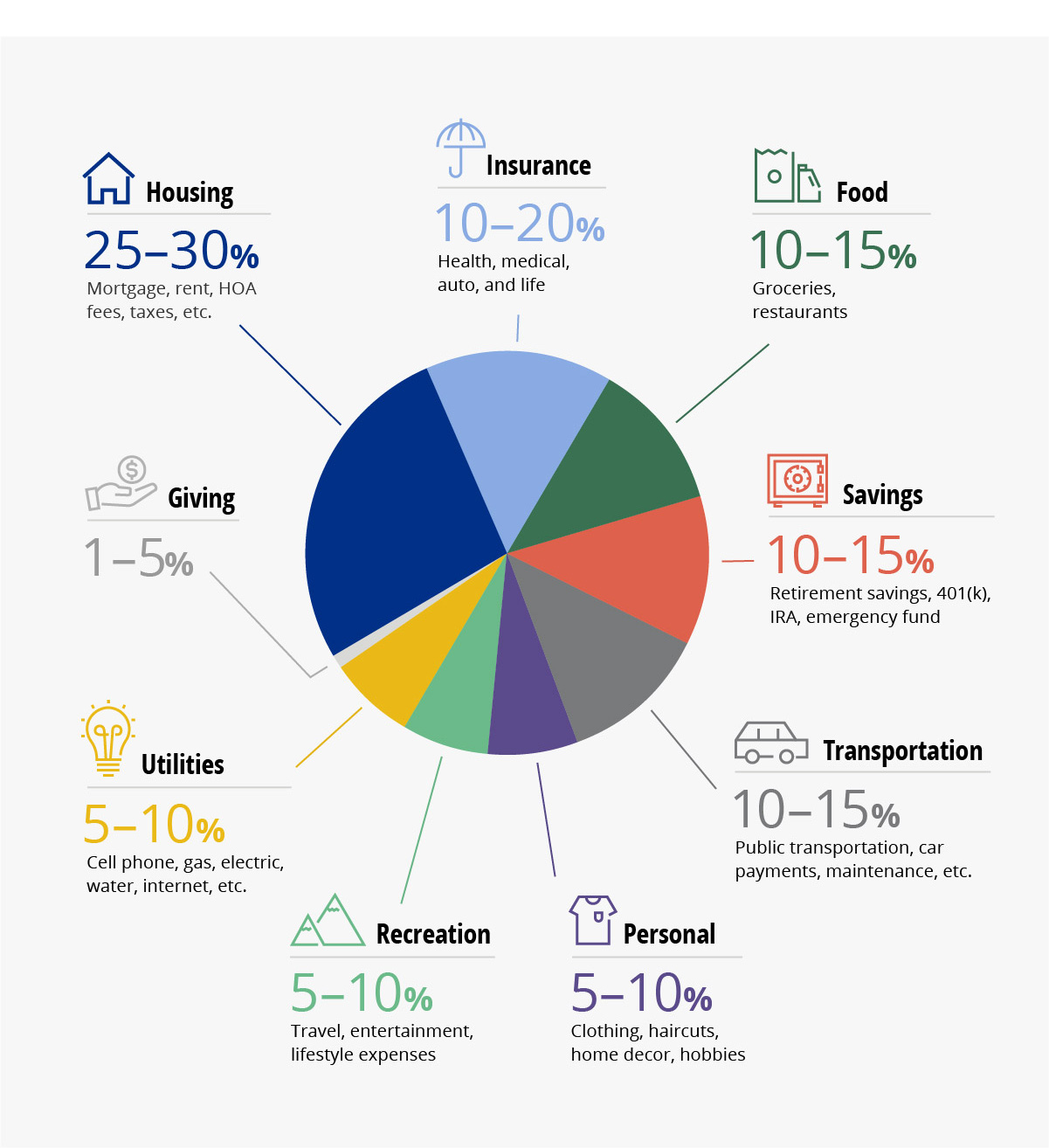

Post-graduation expenses to consider

Rent

If you’re venturing out on your own, housing will likely be your biggest monthly expense. If you’re able to live at home for a little while (without you and your parents getting on each other’s nerves), take advantage of that opportunity to save money. Or look at sharing an apartment or house with a roommate.

If you’re planning on getting a place of your own, you should be prepared to pay both your first and last months’ rent, plus a security deposit. Sometimes, the last months’ rent could count as your security deposit.

Rents vary widely depending on where you live and what type and size of housing you choose. Most likely, your job is going to dictate where you’ll live. But this chart from ApartmentList.com shows median rents for one and two-bedroom apartments as of September 2021. (Median is the midpoint at which half the rents are higher and half are lower.)

City and State |

One Bedroom Median Rent |

Two Bedroom Median Rent |

|---|---|---|

| Delaware |

$1,332 |

$1,644 |

| Arlington, VA |

$2,061 |

$2,495 |

| Baltimore, MD |

$1,107 |

$1,411 |

| Philadelphia, PA |

$1,094 |

$1,268 |

| Washington, D.C. |

$1,817 |

$1,837 |

Rent prices can rise and fall over time. Rent hikes may be more likely if you live in a city with a strong economy, a growing population, high-paying jobs, and a limited supply of rental housing. Some cities and states have rent controls, which cap how much your rent can go up each year.

In addition to the rent cost, you’ll want to consider and ask about these other items before signing your lease:

- How do I pay rent each month (electronically, check, money order, etc.) and how are late fees assessed?

- Are utilities included in the monthly rent cost?

- Is there an additional fee for pets?

- What are the lease renewal options and how many days’ notice do you need prior to moving out?

- What do I need to do to ensure I get my security deposit back?

Furniture

If you’re looking to get rid of your futon and purchase new furniture it could cost you from $3,000 to $5,000, according to ApartmentGuide.com. You could also consider renting a furnished apartment, which is usually more expensive. Add up the cost difference over the course of a year and decide whether it would be cheaper or more financially prudent to buy the furniture up front.

Here are a few tips to help save you money:

- Shop around and compare prices at both traditional retail stores and online shops.

- Search classified, marketplace, and other websites for reduced price furniture.

- Visit local thrift and consignment stores, and consider yard and estate sales as well.

- Look for furniture that's multi-functional, like a dining table that doubles as a desk, and a coffee table with shelves or built-in storage.

- Check around with family and friends, perhaps there’s furniture that they’re no longer using.

In addition, don't forget to budget for other necessities, such as linens, towels, dishes, cookware, and small appliances (think coffeemaker or toaster) that you may need to replace.

Transportation

If you don’t already own a car, it can be more costly than you would expect. If you’re buying a new car, in addition to your monthly payment, you'll have to pay for insurance, repairs, regular maintenance, fuel, and license and registration fees. You may also need to consider parking fees or tolls depending on your commute.

To lower your cost of owning a car, choose an affordable, fuel-efficient vehicle with a good historical resale value, shop around for car insurance, and follow the manufacturer's recommendations for maintenance.

Housing and transportation often influence each other — if your apartment is far away from your job, you may save on rent, but pay more for transportation. An apartment close to your work could be pricier but help reduce vehicle costs.

Insurance

Insurance is a complex financial product that you'll purchase throughout your lifetime. The types of insurance you need will depend on your lifestyle, employment situation, and family status. As a new graduate, some insurance products you should consider include:

- Health insurance (medical, dental, vision)

- Renter's or homeowner's insurance

- Car insurance

How much insurance costs depends on where you live, and the type and amount of coverage you purchase. For example, drivers under the age of 25 pay a premium on their insurance policies. Always shop around, read your policy, and find out how much your copays and deductibles will be if you file a claim.

Other costs

Once you graduate and move into the real world, you may also have other expenses that weren't part of your budget as a student. You can’t anticipate every single expense, but you should budget for student loan payments, travel costs (vacations, visiting family, etc.), and if necessary, professional clothing for your job.

How to save for life after graduation

It's never too soon to start saving for these costs. Spend some time researching your anticipated expenses and creating a financial goal. It might be tempting to end your senior year with some celebratory splurges, but that money could go far in getting you set up in your post-grad life.

5 steps to help save:

- Create a budget and open a savings account.

- While you’re still in school get a part-time job or pick up occasional gig work to boost your savings.

- Save any extra money, from that $10 you found in your pocket to the check you receive as a graduation gift.

- Consider selling your furniture to a younger student rather than giving it away or leaving it behind.

- Pay "rent" to yourself if you live with your parents for a period of time before striking out on your own.

Graduating and moving into the real world is an important transition in your life. Give yourself plenty of time to plan, save, and settle in.