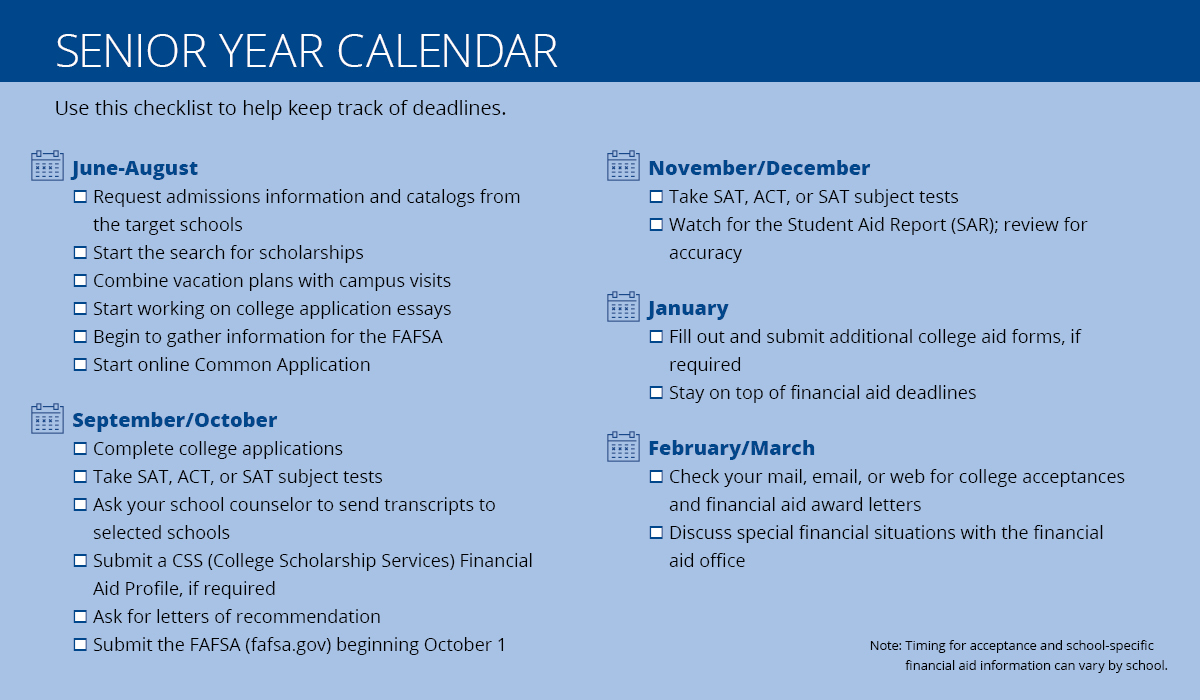

Paying for College: 3 Steps to Help Guide You

The dream of a college degree can come with a hefty price tag. According to Investopedia, the average student debt per borrower is over $35,000. So is it possible to pay for college without taking on massive debt? Follow these 3 steps to discover resources available to help you pay for college.

1. Start with money you won't have to pay back

When paying for college, make sure you maximize "free" money you won't have to pay back, including scholarships and grants. There's money out there if you know where to look.

Scholarships

Most students are aware that scholarships are offered by colleges and universities, but scholarships are also provided by federal and state governments, religious groups, professional organizations, employers, local organizations, and other companies. In addition to academic and athletic scholarships, money can be awarded for:

- Organization memberships

- Community leadership

- Financial need

- Ethnic, religious, or national background

Tip: Check with local organizations in your area to see if they offer a scholarship. And make sure you apply each year you attend college—not just freshman year.

Grants and work-study

Most grants and work-study programs are typically federally funded, so you have to submit the Free Application for Federal Aid (FAFSA ) to apply. The FAFSA is also used to apply for most state loans, grants, and scholarships programs.

- Pell Grants, the largest federal grant program, are based on financial need. The good news: Unlike a loan, a Pell Grant doesn’t need to be paid back.

- Work-study programs are offered by federal and state government, as well as schools. These programs offer part-time jobs that allow you to earn money to help pay educational expenses.

Tip: In addition to the Federal application deadline, the FAFSA also has different application deadlines depending on your state, make sure to double check your state's deadline.

2. Explore federal student loans.

Once you’ve maximized scholarships and “free” money, consider federal student loans to help you pay for college. There are two types of federal student loans: Direct Subsidized Loan, for students with a demonstrated need; and Direct Unsubsidized Loans, which are available regardless of family income.

- You can apply for both types of federal student loans by submitting the FAFSA (Free Application for Federal Student Aid). Check out these important facts to know before applying for the FAFSA (PDF)

- Federal student loans are issued in the student’s name and the student is responsible for paying them back.

- They’re eligible for income-driven repayment plans that link monthly payments to income.

Tip: Federal student loans may be eligible for loan forgiveness programs, such as the Public Service Loan Forgiveness Program for borrowers employed by a public service organization after graduation and forgiveness programs for teachers.

3. Consider a responsible private student loan.

Chances are, you may still need additional funds to help you pay for college. Consider a private student loan. These loans can help fill the gap between your scholarships, federal aid or grants, and federal loans. These loans differ from federal student loans in a variety of ways:

- They’re offered by banks and credit unions.

- They are based on credit worthiness. A lender reviews your credit score and history to see if you qualify. A cosigner─parent, guardian, or other adult, may improve your chances of approval. (Some lenders may offer a cosigner release option in the future.)

- Your interest rate is based on several factors, including your credit worthiness and the loan terms and options that you select.

Tip: Shop around and check into the special features, terms and options, and benefits to help you reduce your interest rate and/or total loan cost.