Credit 101: How to improve your credit score

Good credit is one of the most important elements of a healthy financial life. If you need or want to borrow money, your credit score can make a difference when it comes to whether you're approved and the interest rates you'll pay.

If you've made a money mistake or two in the past (such as paying bills late or defaulting on a debt) your credit score may not be as high as you'd like. But it's possible to raise your score and establish a strong credit profile going forward.

What's in your credit score?

Knowing what makes up your credit score and what affects it is the first step in rebuilding credit history.

FICO credit scores are the credit scores most widely used in lending decisions. These credit scores are based on five factors:

FICO calculates these scores based on the information in your credit reports. Your credit reports — compiled by Equifax, Experian and TransUnion — include key information about your financial activity, such as:

- Who you owe money to and how much you owe

- The minimum payment due on your debts

- Current debt balances

- Available credit limits

- How often you apply for new credit

- How long each account has been opened

Credit reports can include both positive and negative information. Negative information that can take points away from your score includes things like late or missed payments, collection accounts, liens, court judgments, and bankruptcies.

How to improve and rebuild your credit

1. Review your credit report

Aside from knowing what affects your credit score in general, it's helpful to know what's impacting your score specifically. This is where checking your credit reports comes in.

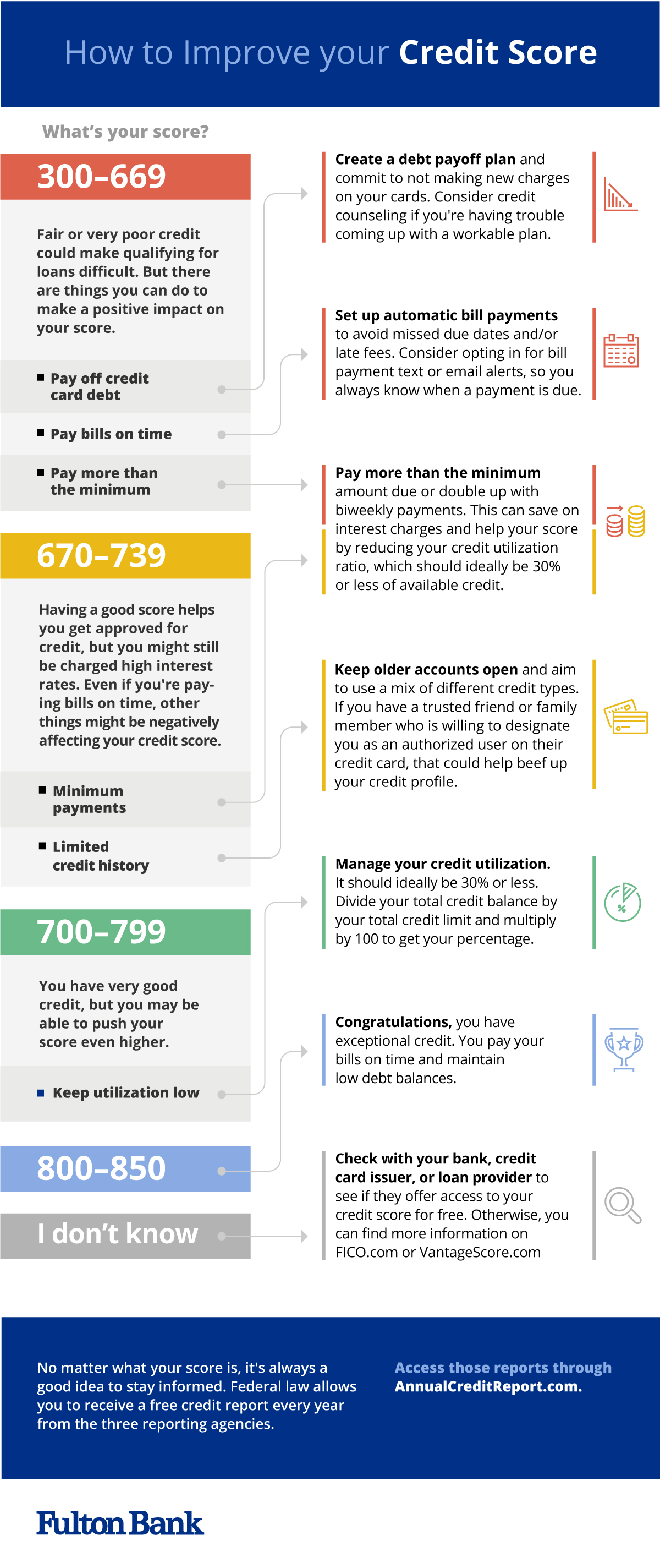

You can get a free copy of your credit report once annually from each of the three credit bureaus mentioned earlier through AnnualCreditReport.com. If you've never checked your credit before, comparing all three reports is useful since creditors and lenders may not report the same information to all three bureaus.

Once you have your credit reports, start by looking for things that could be dragging your credit score down. Again, that means things like:

- Late or missed payments

- Credit cards that are close to your available credit limit or maxed out

- Collection accounts or charged-off debts

- Judgments, liens and bankruptcies

- Frequent inquiries for new credit

This can help you put together a game plan for rebuilding credit because you can target specific areas that need improvement.

While you're reviewing your credit reports, also be on the lookout for errors or inaccuracies that might be hurting your score. For example, if a creditor isn't reporting your payment history or balance accurately, that could work against you for credit score calculations.

Federal law allows you to dispute credit report errors. You can initiate disputes with all three credit bureaus online. When initiating a dispute, be sure to specify what you think is incorrect and why. And if you have any supporting documentation to back up your claim, you can include that as well.

Once your dispute is received, the credit bureau has 30 days to review it. If there is an error, then the credit bureau has to either correct it or remove it. And if the information is shown to be correct, then they have to give you a written explanation of their decision.

If you've identified what's holding you back from having a better credit score and disputed any inaccuracies on your credit reports, you can move on to the next phase of improving credit. There are some specific things you can do here to raise a less than perfect credit score.

2. Commit to paying bills on time

Payment history is the most important factor in credit scoring. If your score is low because of late or missed payments in the past, paying on time going forward should be a top priority.

A simple way to do this is to set up automatic payments of all your bills. But if that's not feasible, you can also avoid missing due dates by setting up recurring payment reminders with your bank or your billers.

3. Reduce debt balances

After payment history, the next most important credit scoring factor is credit utilization. This simply means the amount of your available credit you're using at any given time—the lower this amount is, the better.

If you have debt currently, consider what you can do to make a dent in what you owe. And if you can't pay off a large chunk of debt quickly, you could pursue other options such as a debt consolidation loan or balance transfer credit card.

Opening a new loan or line of credit to consolidate debt can improve your credit utilization ratio. The key is to avoid making new purchases on your old cards once you've cleared those balances.

4. Keep old accounts open and apply for new credit sparingly

Older accounts can help your score if they're factored into your credit age. Keeping older accounts open, even if you've paid off the balances, could potentially add points to your score.

At the same time, you may want to limit how often you apply for new credit lines since each credit inquiry can trim a few points off your score.

What to do next

Improving credit isn't something you can do overnight, so give yourself time to see progress. Checking your credit reports monthly using a free credit monitoring service can help you see what's working (or what's not) as you rebuild credit.

{kind=link}