How Can I Afford a House In This Market?

You’ve been thinking (perhaps dreaming) about buying a home, but the homeownership process (and costs) feels like a daunting task. Even outside of a competitive market, it’s a lengthy process with lots of steps. But don’t let the process stop you. Follow these insights and steps on how to research and find the right home for you.

1. Get smart about common finance and mortgage terms.

Understanding key financial terms helps you make better, more informed decisions about your money-saving options for buying a home.

- Familiarize yourself with terms like prequalification, fixed-rate mortgage, closing costs, and mortgage points so you’re not going in blind. Learn more mortgage terms>>

- Know the meaning (and impact) of the WSJ Prime Rate and how it changes the interest you’ll pay on your mortgage loan.

- Understand the term “debt-to-income” (DTI) ratio. A debt-to-income ratio is calculated with your total monthly debt payments and your monthly gross (pre-tax) income. In addition to your credit score, it’s something that lenders look at when determining whether to lend you money.

2. Set a budget and realistic expectations.

A budget is an opportunity to help you gain more control over your finances. It helps you get clarity on your monthly expenses and pinpoint areas you may be overspending. If you’ve had trouble creating and sticking to a budget in the past, consider these tips:

- Saving is an often-overlooked part of budgeting, but you can't leave it out. When you treat savings like a fixed expense, it's much easier to create and stick with the habit.

- Consider switching to cash or debit-only and leaving your credit card at home so you're not tempted to overspend.

Another important component to be prepared to buy a home is taking an honest self-inventory. Buying a home is considered one of life's big milestones. It's an opportunity to establish your roots in a community, build long-term wealth for you and your family, and it might be a necessity if you're moving to a new area. But ask yourself, why do I want to buy a home and is it the right choice for me now? Am I emotionally (yes, homeownership is an emotional experience) and financially ready? Make sure you’re reviewing your finances, are being candid with yourself, and not rushing into a decision.

3. Improve your credit score.

One of the key elements of qualifying for a mortgage is your credit score. There are many factors that determine your credit score. The three credit reporting companies; Equifax, Experian, and Transunion, maintain historical credit data on individuals that helps determine your score. While the three agencies calculate the score differently there is a general rule of thumb:

- 35% credit history

- 35% payment history

- 30% amounts owned (balances on loans and credit cards)

- 15% length of credit history

- 10% types of credit used (secured and unsecured)

- 10% new credit

It’s a good idea to visit AnnualCreditReport.com and request your free credit report every year. You should review your credit report annually to fix errors so lenders can access your creditworthiness.

If you've made a money mistake or two in the past (such as paying bills late or defaulting on a debt) your credit score may not be as high as you'd like. But it's possible to raise your score and establish a strong credit profile going forward. Solutions include, getting a secured credit card, adding a co-signer, consistently paying bills on time, and working to reduce your debt balances.

4. Focus on reducing debt.

When you're serious about paying off your debt, start by reviewing your budget. First, make sure you have money saved to cover any unexpected expenses. You might hear this referred to as an emergency fund or a rainy day fund. If you don't have one, open a savings account add a regular savings deposit to your monthly budget. After you’ve got an emergency fund established, you can focus on reducing your debt.

- Determine the maximum monthly amount you can use to pay down debt and continue saving onto your emergency fund.

- The snowball and avalanche methods are two methods to consider when paying down debt. Snowball method focuses on small balances first while avalanche pays of the highest interest rate regardless of balance.

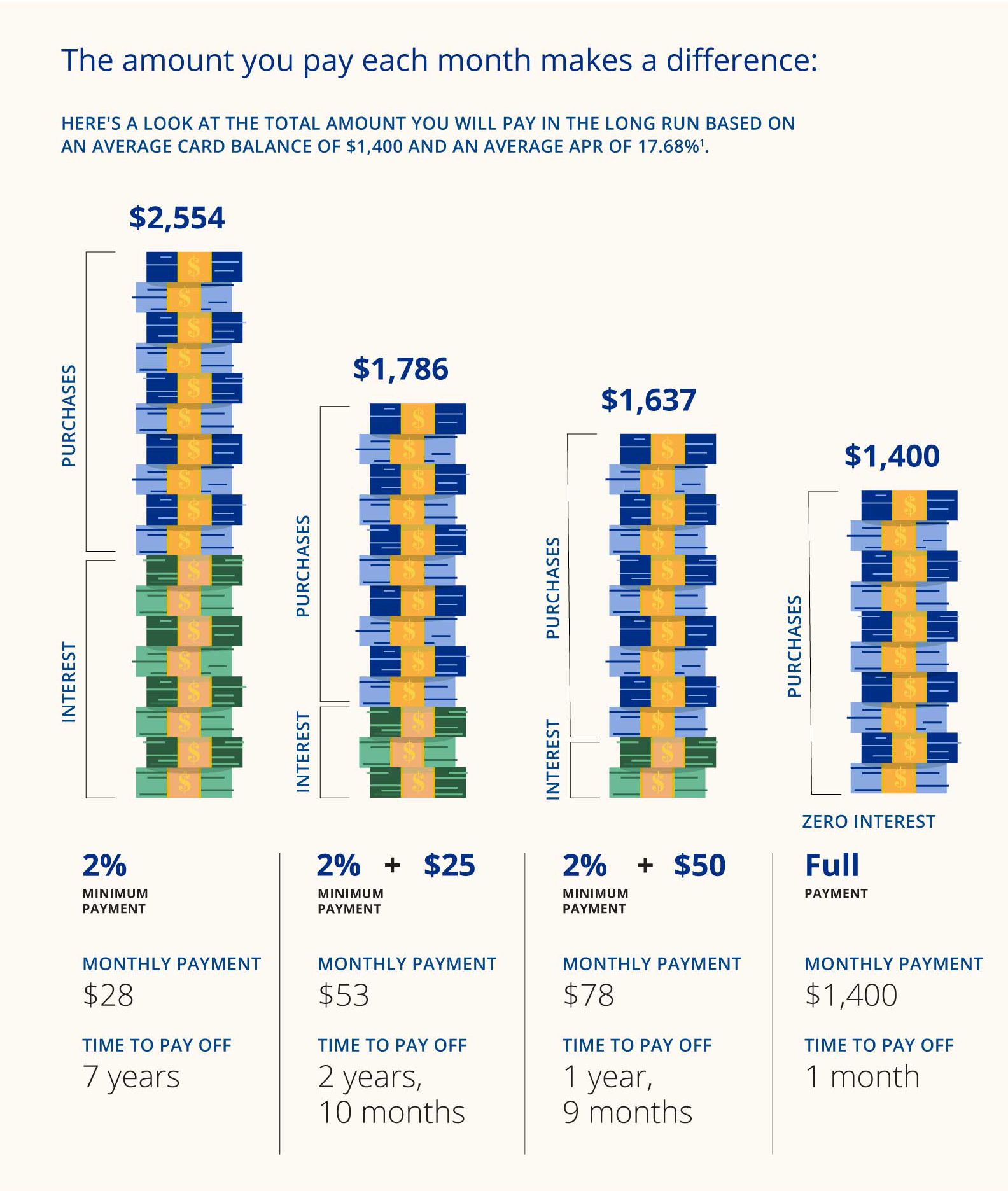

Think strategically. Paying more than the minimum balance has a significant impact on how long it takes to pay off a balance. Here’s an example of the total amount you will pay based on an average card balance of $1400 and an average APR of 17.68%.

5. Explore affordable loan programs.

When it comes to finding the right loan program, it pays to review your options. If you are a first-time homebuyer, or have a low to moderate income, there are programs and services available to help you make the dream of homeownership possible.

- Fulton Bank Community Combo

This special program is a flexible, affordable option designed to meet a diverse range of financial and family needs—including home buyers who have limited funds for a down payment or face unique circumstances. - HomeReady® Mortgage Plus

It’s a flexible, affordable option designed to meet a diverse range of needs including up to 97%1 financing available if you qualify, no Private Mortgage Insurance (PMI) and you do not need to be a first-time homebuyer.

- Closing Cost Assistance Program (CCAP)

In partnership with Operation HOPE, the CCAP program helps make homeownership more accessible by providing up to $2,500 to cover closing costs for mortgages with a loan-to-value ratio of 95% or higher2.

Learn more about additional homeownership programs >>

There are many ways to pursue your dream of owning your own home and tackling the process one step at a time can help make that a reality. Review the steps above to determine if you have the budget, the credit score, and the desire to focus on achieving your goal. The more you’re prepared, the closer you are to getting the keys to your new home.