Downgrade of US Credit Rating

1. Fitch does not have access to superior information or analysis compared with participants in the US Treasury market.

Typically, bond prices react to changes in ratings by the ratings agencies because investors recognize that the agencies have access to information and/or analysis that is not available to investors broadly. In the case of a corporate issuer, analysts at the agencies meet with corporate leaders and may gather information that is not generally available but informs the ratings decision. For many sovereign issuers, the agencies have specialized analysts who know those countries well and may also have access to government officials that is also not available to investors broadly. Even when all information is public, the rating agencies still have some advantage because most investors will not have the resources to analyze all of the information available across numerous countries. Neither of these cases apply to US Treasuries. The vast majority of investors in US Treasuries are well informed, and the US government is very transparent, providing some of the most robust statistical information available for any global economy. Simply put, there is no information in the Fitch report that was not well known to investment professionals. As such, there is no reason to believe that the information in the Fitch report is not already “priced in” to US rates. Indeed, the key rationales for the downgrade cited by Fitch – the growing level of federal debt, the return of debt-ceiling showdowns, and the political disfunction evidenced by the events of January 6, 2021 – were all in the headlines and extremely well known to both professional and retail investors alike.

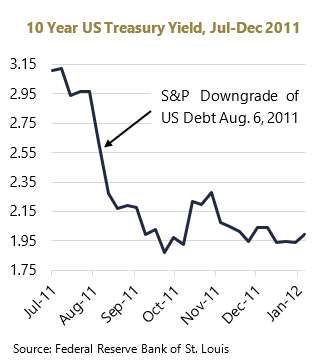

2. Historical precedent indicates that markets do not react to US sovereign ratings.

As noted earlier, Fitch’s competitor S&P downgraded its US sovereign rating from AAA to AA+ on August 5, 2011. In the days and weeks following the announcement, yields on US Treasuries declined, the exact opposite of the impact one would expect from a credit downgrade. The reason was that there was a global flight to quality in August 2011 due to the sovereign debt crisis in Europe. It is frequently noted that the stock market declined right after the S&P announcement, and many attribute this decline to the ratings downgrade. At the time, however, the main challenge facing global markets was actually concerns around potential sovereign defaults in Europe, specifically Greece, Portugal, Spain, and Italy.

3. Following the Fitch announcement last week, US interest rates did increase, but we believe this was due to other news.

Specifically, the US Treasury Department announced plans for debt issuance for the second half of this year that were higher than market expectations. On Monday, July 31, the Treasury announced that planned issuance for Q3 would be $1 trillion, up from $733 billion, and that Q4 issuance would be roughly another $850 billion. This higher level of expected issuance has likely impacted the short-term supply/demand balance in the market as investors plan for second half purchases. Higher than expected federal deficits for FY 2023 are concerning, but given the recently agreed debt ceiling deal, we expect the deficit to decline in FY 2024, which begins in October. Further, continuing strong economic data along with signs of inflation cooling should also help mitigate the near-term fiscal imbalance.

4. Finally, regulatory and compliance concerns should not drive material “forced selling.”

Another concern we have explored is whether there would be meaningful forced selling of US Treasuries or other US-issued AAA securities due to requirements that holdings have a AAA rating. We believe this will not be material for two reasons. First, most if not all rules related to risk assets have an exception for US government bonds, that is the phrasing is typically something like “AAA rated or US government.” Second, Fitch maintained the highest possible country rating for the US at AAA, so municipal, structured, and corporate bonds can still be rated AAA in the US. Typically, the rating agencies will not permit a bond issued in any country to be higher than the sovereign. Fitch is making an exception in this case, which limits downstream effects. That said, the mortgage bonds backed by Fannie Mae and Freddie Mac will likely be treated as rated AA+ by both S&P and Fitch. Thus, there may be some selling in the mortgage market, but this has not been pronounced this week, and markets appear to be functioning as normal.

All in, we believe that markets will absorb this news in stride, and US interest rates will continue to be driven by the macroeconomic data and expectations for how the Federal Reserve will react to it.

Mark Hoffman, PhD, CFA

Chief Investment Officer